Understanding the Car Insurance Claim Process

If you think insurance companies move slowly by accident, you are wrong. Delays are often intentional risk management, not incompetence.

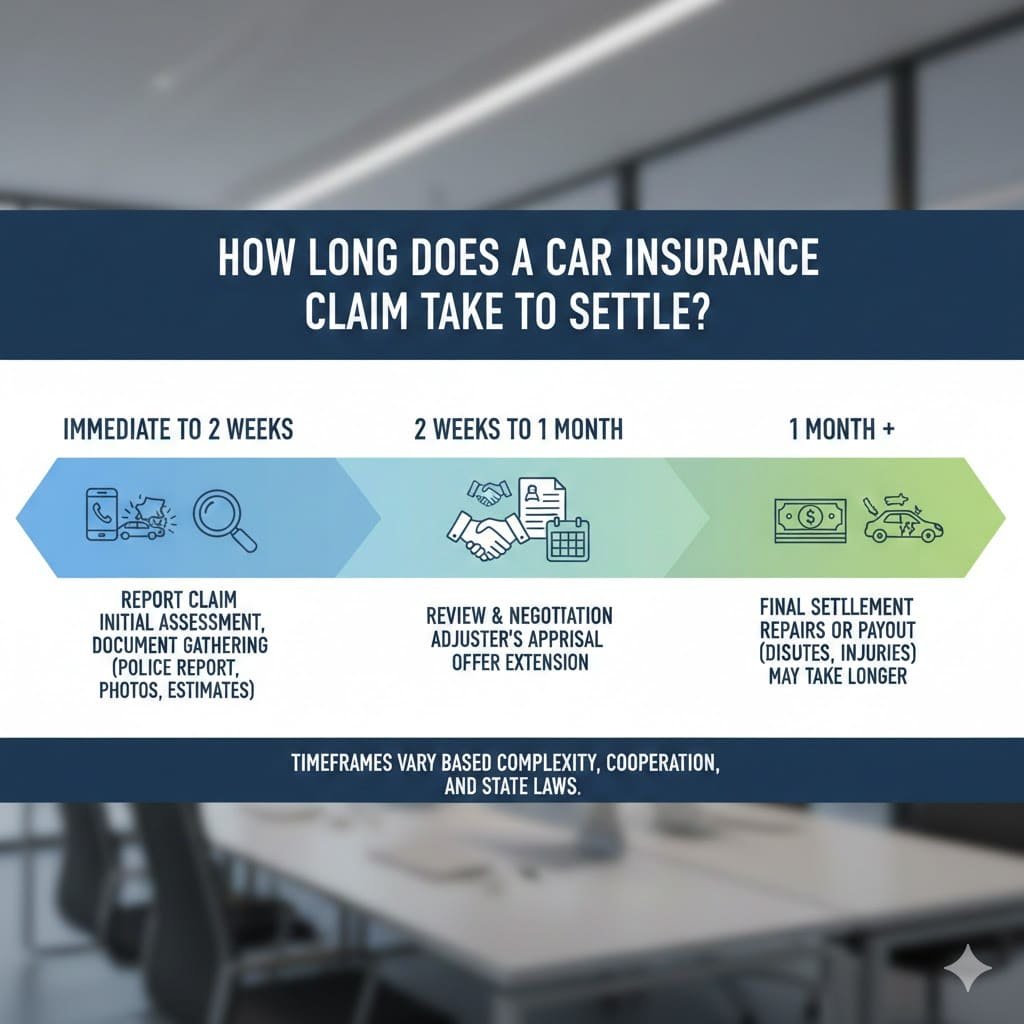

A car insurance claim follows a structured workflow, and every stage affects timing.

Standard Claim Stages

- Accident occurs

- Claim reported

- Claim assigned to an insurance adjuster

- Liability investigation

- Damage and repair assessment

- Medical review (if injuries exist)

- Settlement offer

- Negotiation or payout

Each step adds time. Miss one document and the clock resets.

Average Timeline for Car Insurance Claim Settlement

Typical Settlement Timeframes

| Claim Type | Average Time |

|---|---|

| Minor property damage | 10–30 days |

| Rear-end accident (clear fault) | 2–4 weeks |

| Multi-vehicle accident | 30–90 days |

| Injury claims | 2–12 months |

| Total loss vehicle | 30–60 days |

| Disputed liability | 3–12 months |

If someone tells you “insurance always pays fast,” they are lying or inexperienced.

Key Factors That Decide How Long a Claim Takes

1. Fault and Liability Determination

Liability is the biggest delay factor.

If fault is clear, settlement is fast.

If fault is disputed, insurers slow everything down.

Evidence used to determine fault:

- Police accident report

- Dashcam footage

- Witness statements

- Traffic citations

- Vehicle damage patterns

No police report usually means longer delays.

2. Type of Coverage Involved

Coverage type changes everything.

Fast claims

- Collision coverage

- Comprehensive coverage

Slow claims

- Bodily injury liability

- Uninsured motorist coverage

- Underinsured motorist coverage

Medical claims take longer because insurers wait until treatment is complete.

3. Injury Severity and Medical Treatment

If injuries are involved, insurers do not settle early.

Why?

- Medical costs may increase

- Future treatment is unknown

- Pain and suffering is subjective

Minor injuries settle faster.

Permanent injuries can take a year or more.

4. Total Loss vs Repairable Vehicle

If your car is repairable, claims move faster.

If your car is a total loss, expect delays.

Why total loss claims take longer:

- Vehicle valuation disputes

- Fair market value calculations

- Salvage value deductions

- Title transfer paperwork

Insurers use valuation tools that often undervalue your car. You are expected to challenge them.

5. State Insurance Laws and Deadlines

Each state has its own claim handling rules.

Common state rules include:

- Insurer must acknowledge claim within 7–15 days

- Investigation deadlines (30–45 days)

- Payment deadlines after settlement agreement

Some states penalize insurers for unreasonable delays. Many do not enforce it aggressively.

How Long Does It Take If the Other Driver Is Uninsured?

Uninsured driver claims are slower, not faster.

You must:

- Prove the other driver had no insurance

- Use uninsured motorist coverage

- Often go through arbitration

Timeline:

- Property damage. 30–60 days

- Injury claims. 3–12 months

Uninsured motorist claims are adversarial. Your own insurer treats you like the enemy.

How Long Does a Car Accident Stay on Your Insurance Record?

This affects settlement negotiations indirectly.

- Accident stays on record for 3–7 years

- At-fault accidents increase premiums

- Claims history influences insurer behavior

If you have multiple past claims, expect slower and tougher negotiations.

Why Insurance Companies Delay Settlements

This is the part most guides avoid.

Insurance companies delay because:

- Delays pressure claimants to accept lower offers

- Time reduces claim value leverage

- Many people give up or settle cheap

This is not illegal. It is a business strategy.

How to Speed Up a Car Insurance Claim Settlement

1. File the Claim Immediately

Same-day reporting matters.

Delays raise suspicion and give insurers excuses.

2. Provide Complete Documentation Early

Required documents usually include:

- Police report

- Photos of damage

- Repair estimates

- Medical records

- Proof of insurance

- Driver statements

Incomplete files equal delays. Every time.

3. Do Not Give Recorded Statements Blindly

Recorded statements are used to:

- Minimize liability

- Find inconsistencies

- Reduce payouts

Stick to facts. No opinions. No speculation.

4. Get Independent Repair Estimates

Relying only on insurer-approved shops weakens your position.

Independent estimates:

- Strengthen negotiations

- Expose undervaluation

- Speed dispute resolution

5. Escalate When the Claim Stalls

If nothing moves for 30 days:

- Request a supervisor

- File a complaint with the state insurance department

- Send written follow-ups

Paper trails force action.

When Should You Hire a Car Accident Attorney?

Hire an attorney if:

- Injuries are involved

- Liability is disputed

- Total loss valuation is unfair

- Settlement delays exceed 60–90 days

Attorneys accelerate claims because insurers know litigation costs money.

How Insurance Adjusters Really Work

Adjusters are not neutral.

Their goals:

- Close claims cheaply

- Minimize payouts

- Protect insurer profits

They follow scripts, valuation software, and internal authority limits.

Understanding this helps you negotiate faster.

Negotiation Phase. Why Claims Stall Here

Settlement offers are rarely final.

Common tactics:

- Low initial offers

- “Final” offers that are not final

- Delay between responses

- Repeated document requests

Negotiation can add weeks or months if you push back.

What Happens After a Settlement Is Agreed?

Even after agreement:

- Payment processing takes 7–14 days

- Release forms must be signed

- Lien holders must be paid first

Medical liens slow payouts further.

- Car insurance claim

- Insurance adjuster

- Liability coverage

- Collision coverage

- Comprehensive coverage

- Bodily injury liability

- Property damage liability

- Police accident report

- Claim number

- Deductible

- Fair market value

- Total loss threshold

- Salvage value

- Uninsured motorist coverage

- Underinsured motorist coverage

- Medical payments coverage

- State insurance department

- Settlement agreement

- Claim investigation

- Vehicle repair estimate

- Subrogation

- At-fault driver

Final Verdict

If your car insurance claim is taking:

- Over 30 days for simple damage. That is a red flag.

- Over 90 days with no injury resolution. That is a strategy.

- Over 6 months with clear liability. You need escalation or legal pressure.

Insurance companies do not rush unless forced.