Introduction

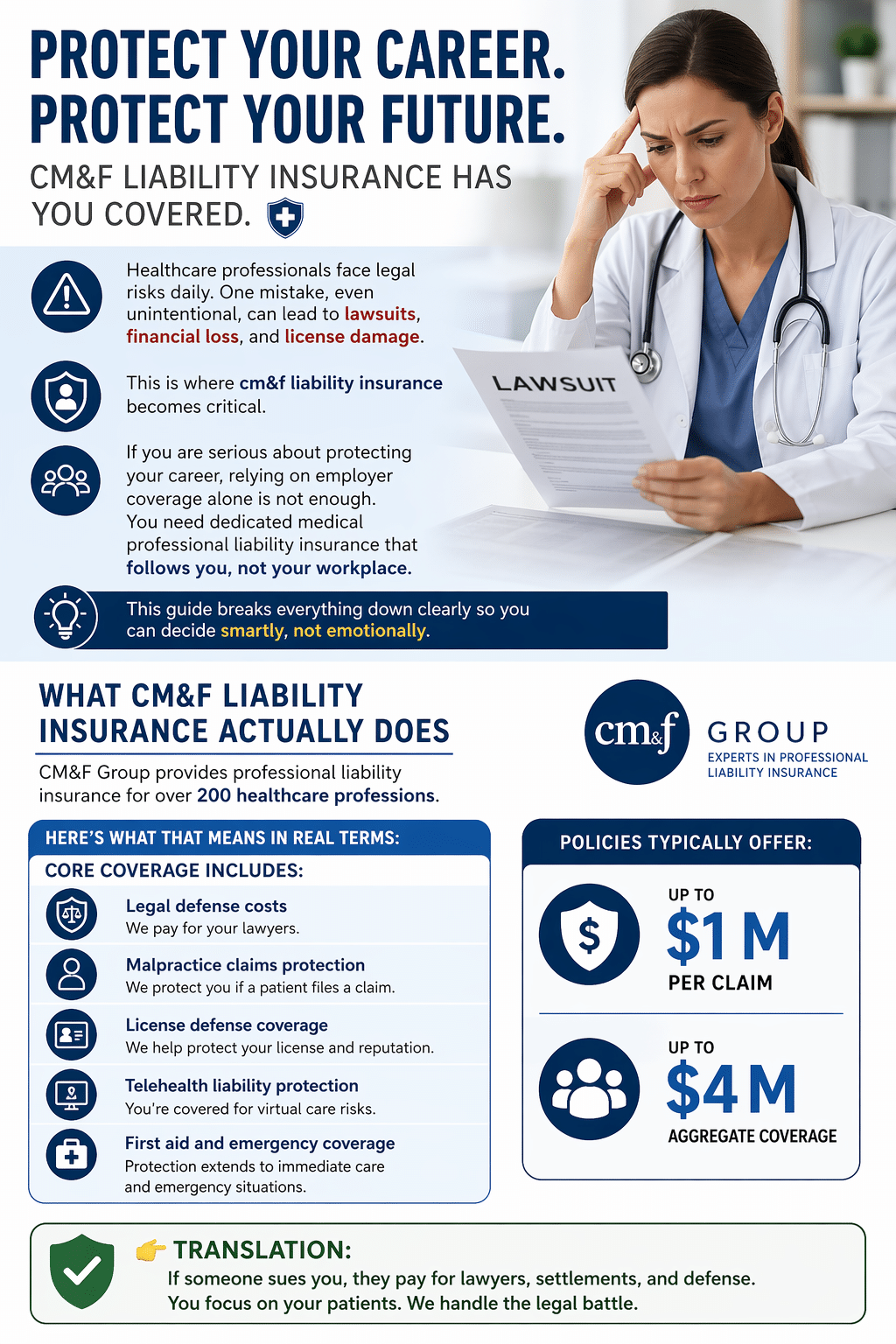

Healthcare professionals face legal risks daily. One mistake, even unintentional, can lead to lawsuits, financial loss, and license damage. This is where cm&f liability insurance becomes critical.

If you are serious about protecting your career, relying on employer coverage alone is not enough. You need dedicated medical professional liability insurance that follows you, not your workplace.

This guide breaks everything down clearly so you can decide smartly, not emotionally.

What CM&F Liability Insurance Actually Does

CM&F Group provides professional liability insurance for over 200 healthcare professions.

Here’s what that means in real terms:

Core Coverage Includes:

- Legal defense costs

- Malpractice claims protection

- License defense coverage

- Telehealth liability protection

- First aid and emergency coverage

Policies typically offer:

- Up to $1M per claim

- Up to $4M aggregate coverage

👉 Translation:

If someone sues you, they pay for lawyers, settlements, and defense.

Types of Coverage Offered

1. Medical Professional Liability Insurance

Protects individuals like doctors, nurses, therapists.

2. Healthcare Liability Insurance

Covers clinics, staffing agencies, and businesses.

3. Malpractice Professional Liability Insurance

Focuses on negligence claims and errors in treatment.

4. Insurance for Healthcare Providers

Covers freelancers, contractors, and part-time professionals.

Pros and Cons (Straight Truth)

| Pros | Cons |

|---|---|

| 100+ years experience | Limited SEO transparency |

| Covers 200+ professions | Pricing not clearly listed |

| Fast online quote (5 min) | Not ideal for all specialties |

| Strong carrier backing (MedPro) | Requires policy understanding |

| Flexible and portable coverage | Some exclusions need review |

👉 Brutal truth:

Good product. Weak marketing clarity.

Comparison with Other Providers

| Feature | CM&F | Typical Competitors |

|---|---|---|

| Experience | 100+ years | 20–50 years |

| Coverage Range | 200+ professions | Limited |

| Online Process | Fast & simple | Slower |

| Pricing | Competitive | Often higher |

| Carrier Strength | A++ rated partners | Mixed |

👉 Key insight:

CM&F wins on coverage flexibility and experience, but competitors sometimes win on transparency and branding.

Why Users Should Buy This Insurance

Let’s be realistic.

You should buy if:

- You work independently

- You do telehealth

- You want personal legal protection

- You don’t trust employer coverage

👉 Reddit insight:

“CM&F… very easy process”

“Affordable and easy to work with”

You should NOT rely on:

- Employer insurance alone

- Cheap unknown providers

- Assumptions about coverage

Real Risk You’re Ignoring

One malpractice claim can cost:

- $50,000 to $500,000+

- Legal fees alone can destroy savings

CM&F policies specifically cover:

- Negligence

- Errors in treatment

- Undelivered services

👉 This is not optional protection. It’s survival.

How liabilitymotorinsurance Fits In

If you are comparing providers, liability motor insurance should be part of your evaluation strategy.

- Use liabilitymotorinsurance to benchmark pricing

- Compare coverage depth

- Analyze exclusions

Most people skip this step and overpay.

Second Use of Brand (Strategic Comparison)

When comparing CM&F with liabilitymotorinsurance, focus on:

- Claim handling speed

- Coverage clarity

- Policy flexibility

👉 Don’t just compare price. That’s how people lose money later.

Third Use of Brand (Decision Layer)

Before buying, use liabilitymotorinsurance as a reference point to validate:

- Whether coverage matches your specialty

- If policy limits are enough

- If exclusions exist

👉 Blind buying insurance is a mistake.

Conclusion

CM&F liability insurance is a strong, proven option for healthcare professionals. It offers flexibility, solid coverage, and strong backing from top-rated carriers.

But here’s the truth:

- The product is strong

- The SEO and content are weak

- Users need more clarity before buying

If you understand your risks and compare properly, this can be a smart investment.

If you don’t, you’ll either overpay or stay underprotected.

FAQs

1. What is CM&F liability insurance?

It is professional liability insurance designed for healthcare professionals to protect against malpractice claims.

2. Who needs medical malpractice insurance?

Doctors, nurses, therapists, and any healthcare provider offering services independently.

3. Is employer insurance enough?

No. It protects the employer first, not you.

4. How much coverage do I need?

Typically $1M per claim and $3M–$4M aggregate is standard.

5. Is CM&F a direct insurer?

No. It works with top-rated carriers like MedPro to provide policies.